Cannabis Rescheduled to Schedule III: What It Really Means for Dispensary ATM Operations

On April 22–23, 2026, the DOJ and DEA moved qualifying state-licensed medical cannabis and FDA-approved marijuana products to Schedule III of the Controlled Substances Act. Recreational cannabis remains Schedule I pending a broader DEA hearing scheduled for June 29, 2026. For dispensary ATM operators and Independent ATM Deployers (IADs), the practical effect is this: banking access will improve gradually for medical operators, but FinCEN compliance requirements remain unchanged, cash continues to dominate dispensary transactions, and ATMs stay mission-critical for the foreseeable future. Section 280E tax relief for qualifying operators is the most immediate financial win, freeing cash flow that can be reinvested into store infrastructure — including modern, compliant ATM equipment.

A Historic Federal Shift With Important Fine Print

For more than a decade, cannabis operators have navigated a painful contradiction: legal under state law, but federally classified alongside heroin as a Schedule I controlled substance. That classification made traditional banking nearly impossible, buried operators under punishing tax rules, and kept dispensaries almost entirely dependent on cash.

In April 2026, that contradiction began to unravel. The U.S. Department of Justice and Drug Enforcement Administration issued a final order reclassifying certain cannabis products to Schedule III — a classification that acknowledges accepted medical use and lower abuse potential compared to Schedule I.

But the details matter, and for ATM operators and dispensary owners, the details determine strategy.

Schedule III applies specifically to FDA-approved cannabis-derived products and marijuana covered by a qualifying state medical license. Adult-use recreational cannabis remains Schedule I. A broader DEA hearing set for June 29, 2026, will determine whether rescheduling extends further — but that outcome is not guaranteed, and planning around it would be premature.

What Schedule III Does and Does Not Change for Banking

Banking has always been the cannabis industry’s most stubborn problem. Prior to rescheduling, fewer than 600 U.S. financial institutions served cannabis-related businesses — a fraction of the total banking system — despite the industry generating billions in annual cash transactions.

Schedule III lowers the federal risk classification for qualifying medical operators. That matters to bank compliance officers who weigh regulatory exposure when deciding whether to onboard cannabis clients. This means more financial institutions may begin exploring cannabis banking relationships, particularly for state-licensed medical dispensaries.

However, the core federal compliance framework has not changed. FinCEN’s 2014 guidance governing Bank Secrecy Act expectations for marijuana-related businesses remains fully in effect. Banks that serve cannabis businesses are still required to file Suspicious Activity Reports, known as SARs, and conduct enhanced due diligence on their cannabis clients.

What is a SAR? A Suspicious Activity Report is a mandatory filing that financial institutions submit to the Financial Crimes Enforcement Network (FinCEN) when they identify transactions that appear inconsistent with normal business activity or raise concerns about money laundering. For cannabis businesses, banks file what are called Marijuana Limited SARs for clients operating compliantly under state law. These filings are not accusations. They are documentation tools that help banks demonstrate regulatory compliance while serving a federally sensitive industry.

For ATM operators, clean transaction records are an important part of this compliance ecosystem. Every ATM transaction at a cannabis dispensary contributes to the paper trail that supports a dispensary’s banking relationship and SAR documentation.

The realistic banking timeline: medical dispensary pilots may begin in Q3 2026, with broader rollout extending into 2027 and beyond. Recreational operators should plan for minimal banking relief in the near term.

The ATM Opportunity Window Is Open — Here’s Why

The gap between where banking is today and where it needs to be is exactly where ATMs operate. That gap is not closing overnight.

Dispensaries across the country continue to process the majority of their retail transactions in cash. Customer preferences, privacy concerns, and the persistent scarcity of banking options all contribute to high cash volumes at the point of sale. ATMs placed inside dispensaries serve a direct function: they give cash-preferring customers immediate access to funds, reduce friction at the register, and measurably lift per-visit spending.

For IADs, the rescheduling moment is not a threat; it’s a deployment window. The operators who secure contracts with recreational and hybrid dispensaries now, while banking normalization is still 12 to 24 months away, are the ones who will lock in the most durable revenue positions.

Deployment Priority by Dispensary Type:

| Dispensary Type | Cash Reliance | ATM Priority |

| Recreational Only | Highest | Critical |

| Hybrid Medical/Adult-Use | High | High |

| Medical Only | Moderate, declining | Medium |

The math on ATM revenue in this environment remains compelling. Surcharge revenue per transaction, multiplied across daily volume, generates consistent returns with relatively low overhead, especially when using a revenue-share model that eliminates upfront capital costs for the dispensary.

280E Tax Relief: The Reinvestment Effect

For IADs, the most underappreciated implication of Schedule III is its impact on dispensary balance sheets.

Prior to rescheduling, cannabis businesses subject to Schedule I classification could not deduct ordinary business expenses under IRC Section 280E. Rent, payroll, marketing, equipment — none of it was deductible. Effective tax rates in some cases reached 70 percent or higher, starving operators of cash flow and limiting investment in their physical locations.

For qualifying medical operators, Schedule III eliminates the 280E burden. Ordinary business deductions are now available. For a dispensary generating $2 million in annual revenue, this can mean hundreds of thousands of dollars in freed cash flow in the first year alone.

What does a dispensary operator do when cash flow improves? They invest in their store. Better layouts, improved customer experience, expanded hours, and modern equipment, including ATMs. IADs who approach newly profitable medical dispensaries with a strong value proposition are entering the conversation at exactly the right moment.

Recreational operators remain subject to 280E until further rescheduling action. That sustained tax pressure actually reinforces ATM value for those operators: ATMs generate surcharge revenue that flows to the dispensary, partially offsetting operational costs without requiring new capital expenditure.

ATM Compliance: What IADs and Dispensary Owners Must Get Right

This is an area where cutting corners can lead to serious exposure. Cannabis dispensaries already operate under heightened regulatory scrutiny, and ATMs placed in those locations inherit that scrutiny. Compliance is not optional; it’s the foundation of a sustainable deployment.

EMV and PCI DSS Standards

All ATMs deployed in the U.S. are required to support EMV chip card technology. Any late-model ATM will meet this standard as a baseline requirement. The current, actively enforced standard is PCI DSS (Payment Card Industry Data Security Standard), which governs how cardholder data is stored, processed, and transmitted.

PCI DSS compliance requires:

- Encryption of cardholder data at the point of capture

- Regular security audits and vulnerability assessments

- Physical security controls on ATM hardware

- Documented incident response procedures

A strong recommendation for IADs and dispensary owners: avoid used or refurbished ATMs. Older machines may not meet current PCI DSS requirements, can be difficult to update, and may carry unknown hardware vulnerabilities. Dispensaries seeking to establish or maintain banking relationships cannot afford the compliance risk posed by outdated equipment. A modern, certified ATM also sends a signal to customers and banking partners alike: this is a professionally operated business.

Cash Loading and Vaulting

Dispensaries and IADs are not required to use armored car services to load ATMs. Private ATM vaulting services are a compliant and widely used alternative. The key requirement is that cash handling is documented, consistent, and traceable. Clear records of who loaded the machine, when, and how much support BSA/FinCEN compliance and protect all parties in the event of an audit or inquiry.

What Is Not Compliant

Cashless ATM systems: Devices that process point-of-sale debit transactions disguised as ATM cash withdrawals using a TID intended for a cash-dispensing ATM are a direct violation of Visa network regulations and are subject to huge fines. These systems have been widely used in cannabis dispensaries as a workaround for card acceptance, but they carry serious legal and financial risk. IADs and dispensary owners should avoid these systems entirely.

The Payment Landscape: ATMs, Debit, and the Card Ban That Remains

Understanding where ATMs fit requires understanding the full payment picture inside a dispensary today.

Cash remains the dominant payment method, driven by customer preference, banking gaps, and the simple reality that not every customer carries the right card for compliant debit systems. PIN debit solutions from specialized processors have gained adoption and offer a compliant path for card-preferring customers, but they operate under their own compliance requirements and do not replace the ATM’s functionality.

Credit card acceptance via Visa or Mastercard remains prohibited. Schedule III rescheduling does not change network rules. Acquirers remain liable for processing cannabis transactions on these networks, and no network policy change has been announced. Any processor claiming to offer compliant Visa or Mastercard processing for cannabis should be treated with significant skepticism.

ATMs occupy a clean, well-established compliance lane that none of these alternatives can fully replace. They serve cash customers, generate surcharge revenue, and operate under a compliance framework well understood by regulators, banks, and operators.

How IADs Should Position Now

The operators who will benefit most from this moment are those who move with clarity and speed.

Immediate actions for IADs:

- Target recreational and hybrid dispensaries first. These have the highest cash volumes and longest ATM dependency. It will be a long time before recreational cannabis is legal like liquor, if ever.

- Lead with compliance credentials. PCI DSS certification, cash handling documentation, and modern equipment

- Offer revenue-share structures that eliminate upfront cost objections

- Educate dispensary owners on 280E relief and how freed cash flow can fund ATM programs

- Build multi-location relationships with MSOs (multi-state operators) for scale

Immediate actions for dispensary owners:

- Confirm medical license eligibility for Schedule III banking benefits

- Maintain ATM contracts through the banking transition period

- Ensure your ATM provider uses current-generation, PCI DSS-compliant equipment

- If vaulting, document all cash handling for BSA/FinCEN purposes

- Consult a cannabis-specialized CPA on 280E amended returns

Frequently Asked Questions

Does Schedule III rescheduling mean that dispensaries no longer need ATMs?

No. Schedule III applies only to qualifying medical cannabis and does not immediately resolve banking access for the majority of dispensaries. Cash remains the dominant payment method, and ATMs continue to serve a critical operational role while the banking landscape evolves over the next 12–24 months.

Are cashless ATMs a compliant option for dispensaries?

No. Cashless ATM systems that disguise POS debit transactions as ATM withdrawals violate Visa network regulations. They are not a compliant payment solution and carry serious legal and financial risk for both the dispensary and the IAD.

Do dispensaries need armored cars to load ATMs?

No. Private ATM vaulting services are an acceptable and widely used alternative. The requirement is documented, traceable cash handling — not a specific carrier type.

What compliance standards must dispensary ATMs meet?

All deployed ATMs must meet EMV chip card standards and current PCI DSS requirements. IADs should deploy only late-model, certified machines to ensure full compliance. Used or refurbished ATMs may not meet current standards and introduce unnecessary risk.

What is a Suspicious Activity Report and how does it affect ATM operators?

A SAR is a mandatory FinCEN filing that banks use to report potentially suspicious transactions. Dispensary ATMs generate transaction records that support a dispensary’s SAR documentation and banking compliance. Clean, well-maintained ATM records are an asset in any compliance review.

Will Section 280E relief affect ATM demand at dispensaries?

Indirectly, yes. 280E relief frees significant cash flow for qualifying medical operators. That capital is available for store investment — including professional, modern ATM equipment. For IADs, this creates a new opening with medical dispensaries that previously had limited reinvestment capacity.

The Bottom Line for ATM Operators and Dispensary Owners

Schedule III is a meaningful federal shift — the most significant in decades. But it is not a banking solution, a payment solution, or an ATM replacement. It is the beginning of a normalization process that will unfold over years, not months.

For IADs, the window to secure strong, long-term dispensary ATM contracts is open right now. For dispensary owners, the ATM remains one of the most reliable, compliant, and revenue-positive tools available while the industry transitions.

Compliance, modern equipment, and clear documentation are what separate operators who thrive in this environment from those who create liability for themselves and their partners.

Ready to deploy a PCI DSS-compliant ATM in your dispensary or expand your IAD portfolio into cannabis locations? Contact ATM Depot for a free site assessment and revenue analysis.

Published April 27, 2026. Sources: DOJ/DEA Final Order April 2026, FinCEN BSA Guidance, PCI Security Standards Council, Marijuana Policy Project. This article is for informational purposes only and does not constitute legal, tax, or financial advice.

Building relationships

Building relationships

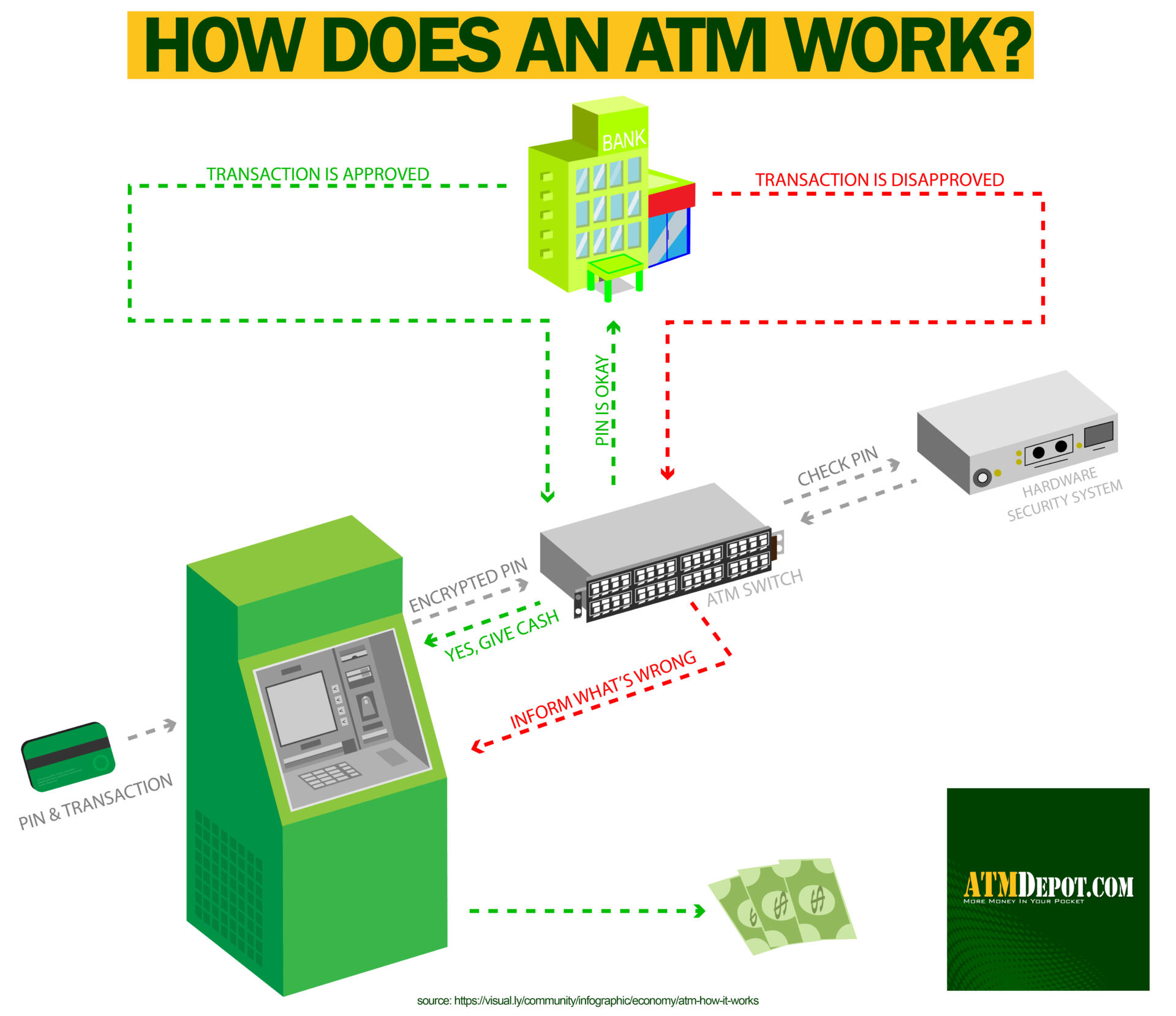

With all the parts covered. Here’s a more detailed look at how an ATM works:

With all the parts covered. Here’s a more detailed look at how an ATM works: